July 26, 2022

By The Delphi Group’s Connor King, Technical Analyst, Climate Change

As many parts of the world grapple with another summer of extreme temperatures, getting to net zero is something we all need to get our heads around. As a first step, many organizations measure and report their greenhouse gas (GHG) emissions (otherwise known as their “carbon inventory”). This helps them figure out the biggest opportunities to reduce their climate impact.

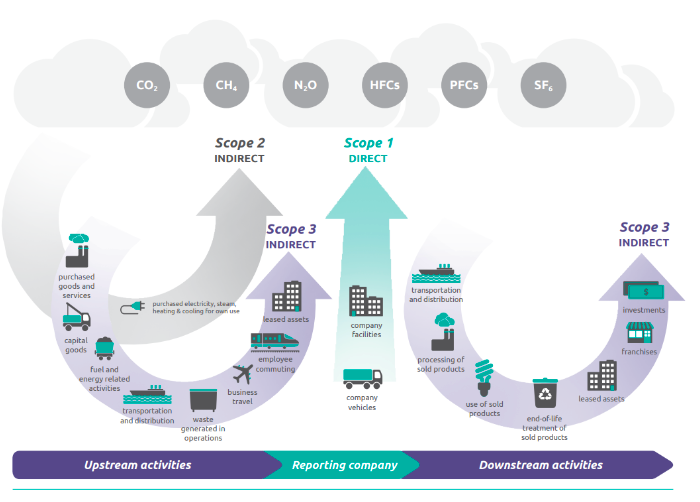

The question is, what should your company be including in your carbon inventories? A majority of companies stop at the emissions associated with activities that they have direct control over, namely:

The conversation we’re all having in 2022 is about the importance of counting the emissions associated with activities that happen OUTSIDE of your organization but that are connected to your organization through its value chain – your scope 3 emissions. These include the emissions associated with creating the products you purchase, distributing the products you produce, your investments, and employee activities such as commuting and business travel. Because you don’t directly control them, they’re the most difficult to track and manage. But that doesn’t mean you shouldn’t do it.

Scope 1, 2 and 3 emissions

Source: GHG Protocol Greenhouse Gas Protocol Corporate Value Chain (Scope 3) Standard.

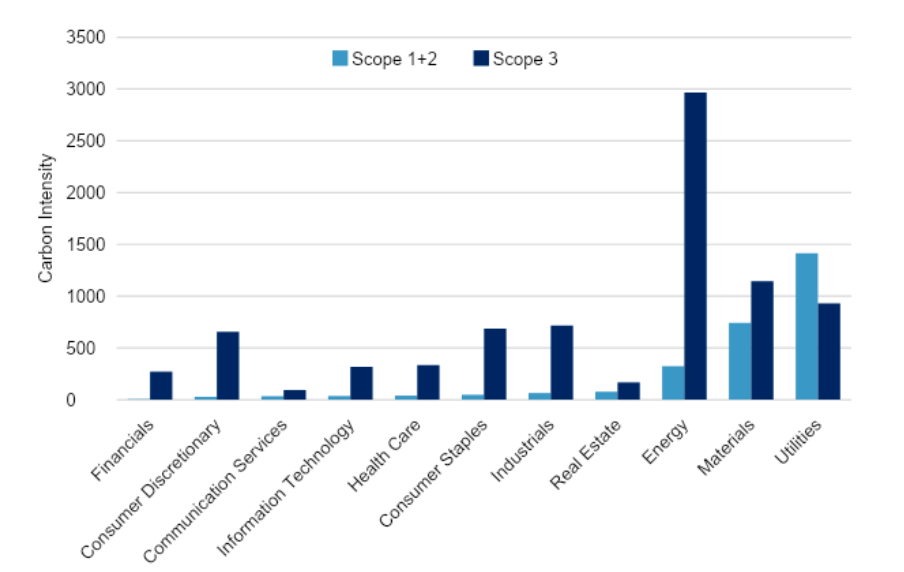

For most companies, scope 3 emissions will make up the majority of their carbon footprint. A 2020 CDP report on suppliers across 12 industries found that upstream scope 3 emissions alone were 11 times greater than their scope 1 and 2 emissions combined. Just think of the oil and gas sector. Yes, there are emissions associated with the extraction and processing of fossil fuels, but most of the emissions occur when people use that fuel to run their cars or heat their homes.

Another example is the retail sector. The emissions of a single store might be insignificant, but the emissions associated with making and transporting the products to the store, consumer use, and the eventual disposal of the products they sell means that up to 98% of a retailer’s carbon footprint can be scope 3.

Comparing scope 1, 2 and 3 emissions by industry

Source: S&P Global, December 2020.

If we don’t measure and manage scope 3 emissions, it’s going to be really hard to get to net zero by 2050.

We’re not the only ones who think so. Sure, scope 3 was historically treated as an afterthought in GHG inventories. But now? Proposed mandatory disclosures by the U.S. Securities and Exchange Commission (SEC) would require scope 3 reporting where these emissions are material (i.e., where there is “a substantial likelihood that a reasonable investor would consider them important to a voting or investment decision”) or where scope 3 emissions are included in a publicly stated GHG target. In addition, the Science Based Targets Initiative (SBTi) now requires a scope 3 reduction target when scope 3 is more than 40% of a company’s total emissions.

Market forces are increasingly driving change as well. The Partnership for Carbon Accounting Financials’ (PCAF’s) GHG Accounting and Reporting Standard for the Financial Industry requires reporting on emissions attributable to lending and investing activities. PCAF already requires reporting on scope 3 financed emissions from the oil, gas, and mining sectors, and by 2026 all sectors will be covered. Going forward, this means that financial institutions will increasingly face pressure to reduce lending/investment in organizations with significant scope 3 exposure.

We’ve noticed these shifts at Delphi. Increasingly, clients are coming to us for help with their scope 3 reporting to meet investor expectations or the demands of other stakeholders. The combination of market forces, climate risk/opportunities, and regulation means that organizations serious about sustainability can no longer ignore scope 3.

Rome wasn’t built in a day; your scope 3 inventory won’t be, either. It’s a big undertaking so we typically recommend a phased approach to our clients.

Step 1: Identify the scope 3 categories that are most relevant to your organization

There are a LOT of categories of scope 3 emissions, so the critical first step is identifying which ones are relevant to your organization. Business travel or purchased goods tend to be relevant to most organizations, while others, like the use of sold products, are only relevant to a few.

This scope 3 screening serves a second, but equally important purpose: it brings together various internal stakeholders who are key to the overall inventory. Setting a strategy for data collection and responsibilities early on – and making sure everyone is on the same page – will really set you up for success here. During our recent work with a mid-market financial institution, we brought stakeholders together to provide background on the scope 3 process and align on a vision going forward. From day one, this created a united front across different departments and helped them run an efficient process.

Step 2: Estimate your scope 3 emissions to figure out the biggest opportunities for reductions

The next step is quantifying your scope 3 emissions. Data gaps are often a reality at the beginning of the scope 3 process, so we typically recommend a spend-based approach. Spend-based models link economic output and emissions on a sectoral basis. Essentially, every dollar you spend has an associated emissions value, and this model uses accounting data to estimate the emissions associated with various scope 3 activities. This means that data gaps are rarely a barrier to starting your scope 3 journey.

While spend-based models are great for when you can’t access data, they aren’t highly accurate. Instead, the results of these models can help you do an “order of magnitude” estimate – that is, figure out where emission hotspots exist, provide an approximation of emissions, and identify which categories are worth quantifying at a more granular level.

The GHG Protocol identifies a hierarchy of quantification approaches for each scope 3 category, from most to least accurate. Spend-based is usually the least accurate. Next there is the average data method, which usually makes use of weight-based data, such as how many kilograms of steel you purchase. Finally, supplier-based methods allow you to directly engage with your value chain to get business-specific data, which can help drive deep reductions in targeted hotspots. While you might not want to develop your entire sustainability strategy for the next 10 years around the spend-based approach, it’s a great place to start the measurement process.

Step 3: Quantify your emissions and develop your reduction and data improvement strategy

Once you’ve identified your scope 3 emissions hotspots, the real fun begins. From the outset, having a clear idea of where you want to drive emissions reductions is critical. This usually involves identifying one to two major emissions sources in your value chain to focus on. For most organizations, these categories will be very clear.

Reducing scope 3 emissions is inherently tied to improving data quality. As previously mentioned, while spend-based models provide a good approximation, they are not very useful once you try to start making reductions. Think of any business which purchases commodities: when prices go up (as many have due to the COVID-19 pandemic and supply chain issues), so will a company’s spend. Remember that in spend-based models each dollar spent has an associated emissions value. So, even if the company does not purchase more of the commodity, they are still spending more because prices have risen, which means their emissions will increase on paper when in actuality they haven’t changed. Clearly, data quality needs to be refined if emission reductions are going to be tracked in any meaningful way.

For most organizations, this means moving to the previously mentioned average-data or supplier-based approaches (i.e., making use of weight or business-specific data). We recently helped a large retail client switch from a spend-based to an average-data model, and they were surprised at how their emissions profile changed. For the first time, they could see the outsized impact that certain product purchases had on their scope 3 emissions. The data insights gained from moving to a more refined model allow for real strategy development. In our client’s case, this means they can now consider material substitution and ecodesign on a level that previously hadn’t been possible.

As data systems become more refined over time, companies can develop increasingly sophisticated strategies for reducing their emissions.

With the rise of emissions reporting regulation and voluntary standards, scope 3 is not going away anytime soon. If you’ve already begun your organization’s scope 3 journey, fantastic! If not, it’s never too late – we hope you’ll join us in our efforts to create a sustainable and just future within a generation.

Connor King is a Technical Analyst, Climate Change for The Delphi Group. Delphi’s blend of expertise in life cycle analysis, carbon accounting, and sustainability strategy make it uniquely suited for scope 3 inventory work. For more information on how The Delphi Group can help you with your net-zero goals, reach out to Connor at cking@delphi.ca