November 20, 2023

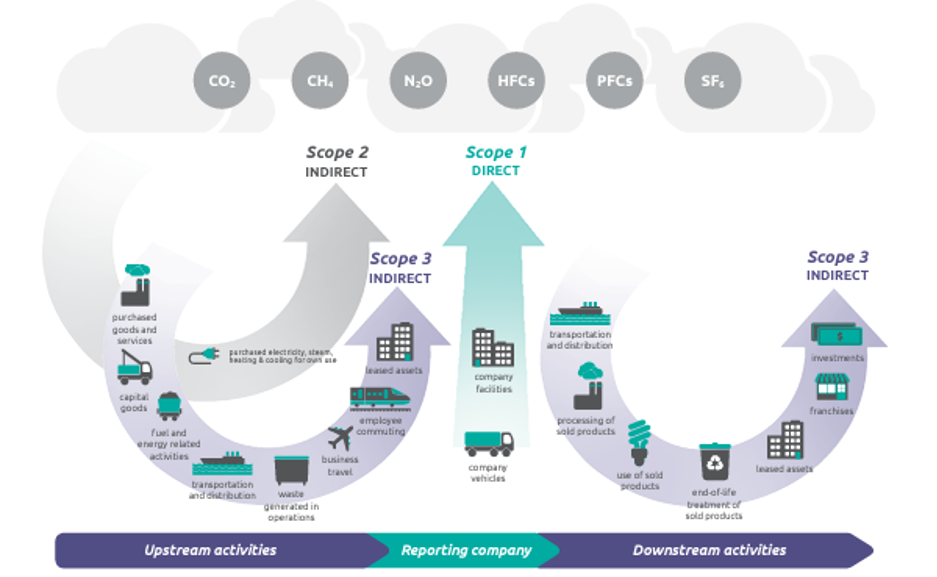

In response to the rapidly accelerating climate crisis, organizations are prioritizing climate-related risks and opportunities and building them into their business strategies. This journey often starts with quantifying the original greenhouse gases (GHGs) of corporate inventories: scope 1, which are direct emissions that result from sources that are owned or controlled by an organization, like those associated with operating a boiler or driving vehicles; and scope 2, which are indirect emissions primarily from generating electricity that is purchased by an organization.

The relatively new kid on the block is scope 3, which are emissions representing the entire value chain of an organization. They include everything from employee commuting to purchasing to what happens when consumers buy your product.

In this blog, we’ll debunk common myths about measuring and reporting scope 3 emissions so that you can go further and faster on your climate journey.

An organization’s scope 1, 2, and 3 emissions according to the GHG Protocol. Source: GHG Protocol Corporate Value Chain (Scope 3) Accounting and Reporting Standard.

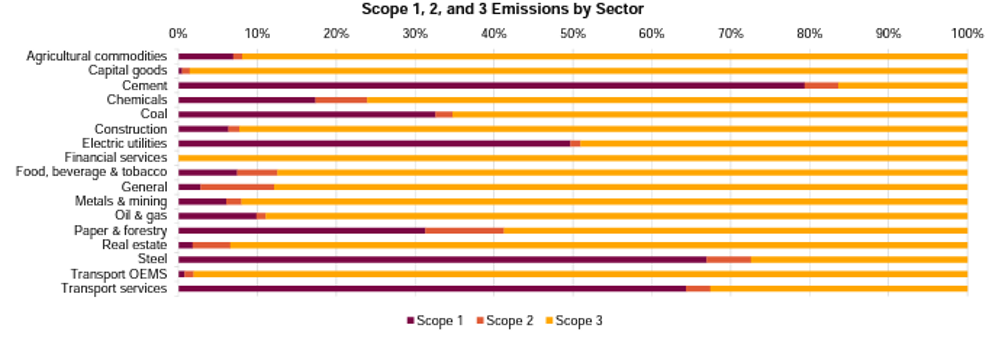

Scope 3 is the largest category of emissions for most companies. In fact, it accounts for 75% or more of emissions for many organizations. The exceptions are sectors that require significant energy use to deliver a service (e.g., transportation), or that use significant energy and/or GHG-producing chemical processes to produce durable building materials (cement, steel, wood) or secondary energy types (thermal electricity). Check out the breakdown for your industry below:

Source: CDP Technical Note: Relevance of Scope 3 Categories by Sector

Given the relative size of scope 3 emissions in many corporate carbon footprints, addressing these emissions is critical to making progress against your climate goals.

The GHG Protocol defines 15 categories of scope 3 emissions (see below), and that can feel overwhelming when you’re starting out on your reporting journey. A common misconception is that ALL 15 emissions categories apply to every organization. The good news is that you can limit your reporting to relevant scope 3 categories.

Scope 3 categories

So far so good, but how do we assess relevance? Follow guidance provided in the GHG Protocol’s Scope 3 Accounting and Reporting Standard, which includes these considerations:

The general rule of thumb is that an emission category is relevant if it contributes significantly to your scope 3 emissions. However, as noted above, other factors can also make an emission category relevant to an organization, regardless of size. Take waste generated in an organization’s operations (category 5) as an example. Even if it’s not a significant emission source, it may be considered relevant if under scrutiny by stakeholders like the general public.

Expert tip: Before starting a relevance assessment, streamline your work by identifying and removing any categories that may not apply to your organization. For example, if you’re a professional services firm that doesn’t manufacture or sell products, categories 10 (processing of sold products), 11 (use of sold products), and 12 (end-of-life treatment of sold products) are likely not applicable.

This one is not entirely a myth: Under the WRI/WBCSD GHG Protocol standards, reporting scope 3 emissions still remains voluntary. However, there has been a shift over the last decade. Regulatory and investor pressures — as well as disclosure mandates set by countries, legislatures, and other governing entities — are pushing organizations to quantify and report on scope 3 emissions. Examples include:

Scope 3 reporting requirements are becoming more common and robust. Assess your risk by looking at peers in your sector: if they are reporting scope 3 emissions and you are not, your organization could face a reputational and market risk.

Data collection is one of the biggest hurdles organizations face when completing a high-quality scope 3 inventory. Unlike with scope 1 and 2 emissions, collecting data for a scope 3 inventory involves more extensive internal and external engagement, making it more time and labour-intensive. Obtaining high-quality data for certain scope 3 activities may be practically impossible.

The GHG Protocol recognizes this challenge, which is why the Scope 3 Standard offers various methods for estimating these emissions. The methods have varying degrees of specificity:

Generally speaking, more specific methods require more time and labour but produce higher-quality scope 3 results.

Let’s look at another example: The least specific approach for estimating Purchased Goods & Services (category 1) emissions is the “spend-based” method. This relies on annual spend data for purchased goods and services, along with emission factors from publicly available databases that provide average emissions per dollar spent across different economic activities. For more specific estimates, organizations can use the mass or quantities of goods purchased, coupled with relevant average emission factors (e.g., average emissions per unit of goods produced or service provided). Even more specific methods involve obtaining emissions data directly from suppliers.

So, how do you choose the best estimation method for each scope 3 category? The GHG Protocol recommends these criteria for deciding when more specificity is needed:

You don’t need the most specific method in all cases, and certainly not when you are just starting out. In fact, we recommend that you start with a scope 3 screening exercise, which uses lower-specificity methods, such as spend-based or average-data methods, for all applicable categories. The resulting “order of magnitude” tallies certainly have their limitations, but they can help you cost-effectively determine where additional investments in specificity will yield the greatest returns.

For many organizations, scope 3 remains a complex and unfamiliar area of their corporate inventory. Some organizations question how relevant scope 3 emissions are to their climate strategy, stakeholder expectations, and reporting obligations. Many are concerned about access to high-quality data and the effort and cost associated with data collection. Most are unsure about how best to influence these emissions once they have been assessed.

Delphi has been working with clients for over a decade to quantify and disclose their scope 3 emissions. With the right approach, it’s possible to generate useful results in an efficient and credible way that can meet your needs… AND help drive the kind of economy-wide, cross-sectoral changes we need to tackle the climate crisis.

Farr Fatemi is a Director and Nimrah Anwar is a Consultant at Delphi. Contact Farr at ffatemi@delphi.ca or Nimrah at nanwar@delphi.ca